ABC analysis (always better control)

Concept and need:

- In inventory management, ABC analysis plays a vital role. It is an analysis of the range of items divided into three categories.

A- Extremely important items

B- Average of important items

C- Relatively unimportant items - Therefore, the items in our inventory can be classified into the above three categories. 'A' item types receive more attention than category B. Category 'C' item types receive less attention as they are relatively unimportant.

- ABC analysis is also called Always Better Control. The reason is that all items do not have the same status in the inventory. If the same attention is given to everyone, then the most important items may suffer (i.e., the production flow may be seriously disrupted) or the less important items may receive unnecessary care (which is not necessary).

- Any organization usually deals with many items. It is very difficult to exercise control over all items. Control means transactions related to inventory, degree of control, type of records to be maintained, batch sizes, frequency of review, size of safety stock to be maintained, etc.

- ABC analysis helps to classify thousands or even millions of individual items into three groups, namely items belonging to group A, group B and items from group C respectively. ABC analysis is based on the Pareto Principle.

- The consumption value is the basis of the ABC classification. Consumption value is the product of unit price and consumption.

ABC classification mechanism:

Steps involved:

1. Collect the previous year's consumption and the unit price of each item.

2. Multiply the consumption and the unit price of each item to obtain the consumption value.

3. Sort the items corresponding to the consumption value.

4. Calculate the accumulated consumption value for each item.

5. Find the percentage of the accumulated consumption value.

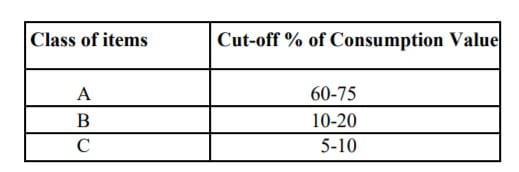

Typically, to classify items into class 'A', there is leverage available. Leverage is 60 to 70 percent of the consumption value.

This means that the cut-off value can be set at 60 to 70 percent of consumption and the corresponding items that contribute to the cut-off value are classified as class items.

Likewise, to classify items in class B, there is a consumption value leverage in the range of 10 to 20 percent of the consumption value. To classify items in class C, there is a consumption value leverage in the range of 10 to 20 percent of the consumption value.

ABC Percentage

ABC PercentageControl types

The objective of classifying items in ABC is to control each item. The degree of control required for class A is not the same for items in classes B and C. The following table assists the materials manager in the type of control to be exercised over these items.

STEPS TO DO ABC ANALYSIS

1. Prepare a list of all items and estimate your annual consumption.

2. Determine the unit price for each item.

3. Get the annual consumption in rupees by multiplication.

4. Arrange the items in descending order.

5. Calculate the accumulated annual usage and number of items in %.

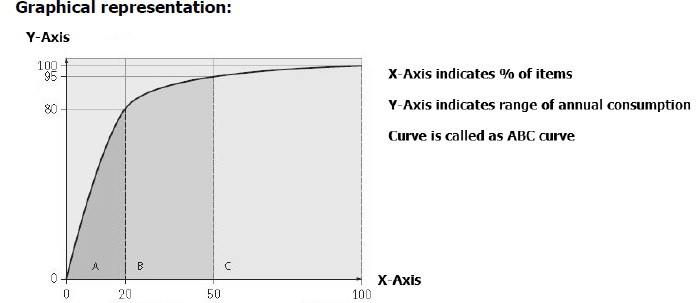

6. Draw the graph.

7. Sort into categories A, B, C.

8. Decide inventory control policies.

ABC Analysis Chart

ABC Analysis Chart Important considerations in ABC analysis:

1. The ABC curve has a similar shape for different industries.

2. All items that the company consumes must be considered together. The ABC curve is common for all types of materials in the

3. Consumption of goods can be annual, monthly or applicable for any period.

4. Some categorization like A1, A2, B1, B2, C1 and C2 may be possible if required.

Managing inventories by ABC:

ABC analysis is the method of ranking the items involved in a decision situation based on their relative importance. Its classification can be based on monetary value, availability of resources, variations in delivery time, criticality of the part for the operation of an installation, new customer parts exclusive to that product and others.

Cyclical inventory can be managed through ABC analysis:

“A” value items should be counted more frequently, that is, once a week to accurately monitor these items, which has a greater impact on the inventory value. “B” value items can be counted once a month because they are moderate value items that have less impact on inventory value. “C” items should be counted once every three to six months because they are less consumed value items and have much less impact on inventory value.

The obsolescence budget also takes into account the management of ABC analysis.

“A” items have the greatest impact on the budget if they are considered obsolete and discarded from inventory. These parts can mislead the reviewer because “A” parts may not be used for several years, but because of their critical importance they may be needed later. The slow activity report would not detect this need. Warehouse management and management need to consider all aspects of parts before they are discarded and become obsolete. ABC analysis provides a perspective that enhances this decision making.

Another use of ABC analysis is in the reorganization of the warehouse.

Annually, a review of parts storage areas must be carried out by the warehouse manager. In this analysis, ABC coding must be considered so that the “A” pieces are continually moved to the lowest areas or areas that are easiest to access. 'B' items should be moved to intermediate areas and 'C' items placed in all other areas of the stores.

Advantages of ABC analysis:

1. Better exercise of control over all materials.

2. Capital invested in inventories can be reduced to minimum levels.

3. Storage and storage costs can be reduced.